Estate Planning

Estate planning ideally involves an estate planning lawyer, a tlnancial advisor, and an

income tax accountant.

Two prime concerns in all plans are providing for incapacity and death. Estate taxation is not

as great a problem now with the current exemptions well over $12,000,000).

Lifetime planning/or incapacity uses powers of attorney and living trusts. Planning should

include the possibility of incapacitated spouse or children. Health care documents (medical power

of attorney and directive to physicians) are indispensable for peace of mind. Property powers of

attorney are useful with certain exceptions.

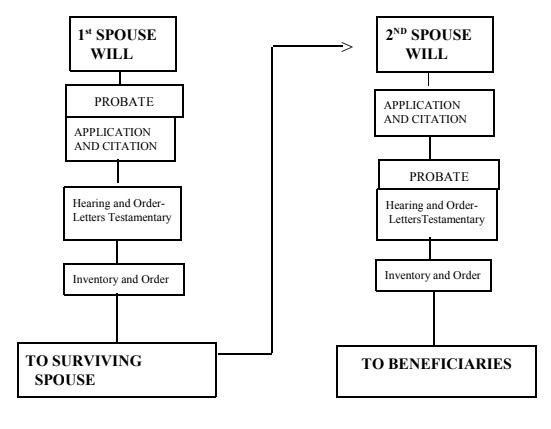

Lack of death planning results in intestacy (no will..no trust). The result may be a court-

supervised administration, an expensive process. Planning to avoid intestacy at death typically

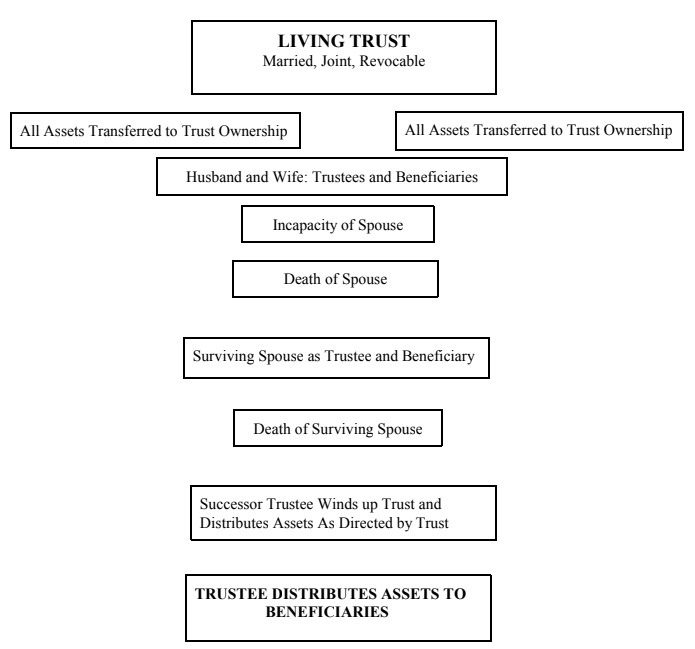

involves the use of living trusts or wills. Wills require court action at death to become effective.

Revocable trusts are private and involve no courts. Both vehicles accomplish the same result,

although probate of wills at death involves lawyer expense for the necessary probate court action. While a trust requires lawyer expense as well to draft the trust agreement and transfer (re-title) assets into the trust. Calling a trust a “living” trust is merely saying trhe the trust is revocable. A trust is presumed revocable unless the instrument creating it provides otherwise.

Not all assets are subject to the probate process that a will requires . Examples: usually life

insurance, annuities, and retirement plan benefits are governed by their own contract, not a will.

Tax-favored funds such as retirement accounts can be efficiently distributed, also, to the ultimate beneficiaries through a revocable trust but, ideally, not through a will probate.

Clarity of expression is the key to successful transfer of assets at death whether the

vehicle is a will or a living trust. Immature (by age or judgment) children can be protected from

wasting assets by use of trusts to insulate the assets from poor judgment. Trusts are a tool for

controlling assets after death while providing financial security for the beneficiary.

Revocable trusts are one way to control assets upon incapacity and to distribute assets

at death because they are private (do not depend on probate court approval) and provide for

continued management of assets upon incapacity.

Both living trusts and wills can include estate tax planning, but with the basic estate

tax exclusion amount now at $17 million, most do not need estate tax avoidance provisions in their plans.

The gift tax in brief: Each calendar year each person may give Lu as many non-charitable

donees as much as (this year’ s) $17,001.00 (the “annual exclusion” amount, indexed for inflation) before a US gift tax return is required. However, a gift tax is not payable unless the aggregate of all gifts that were greater that the annual exclusion amount exceeds the basic exclusion amount of $12.92 million [adjusted for inflation for 2023. The basic exclusion amount might be decreased by Congress. It is scheduled to “sunset” [ revert back to 2001 amount of $1 million]. All exemptions are up for grabs since Washington is always looking for tax money.

A comparison of the expense of estate planning with wills (ani probate) versus trusts can be

summarized this way: two wills and two probates will be at least 33% greater in expense than a joint married trust.